Money, made kinder.

A financial wellbeing product built from the same research it was designed to move.

Mental and physical wellbeing already had a home. Money didn't.

LifeWorks (now TELUS Health) ran one of the largest employer-paid wellbeing platforms in Canada. The mental side and the physical side were already mature surfaces. The financial side, the one employees were the most stressed about and the least willing to talk about, was missing.

I led design on the product that filled that gap: myFinances, a desktop web experience offered to Canadian employees through their employers. The brief from product leadership was simple. The same internal research team that published the quarterly Financial Wellbeing Index™ had a 30-page report on what was breaking in Canadians' financial lives. The product had to actually move those numbers.

The research wasn't hypothetical. It was a 64.0.

The internal Financial Wellbeing Index™ surveyed 3,000 working Canadians every quarter. By Summer 2022 the overall score was 64.0, the lowest since the Index launched in 2021. Of the four sub-scores, financial perception (how people felt about money) had fallen the sharpest.

Five numbers from the report shaped the brief.

Each of those numbers had a person attached: a 28-year-old gig worker, a 45-year-old single parent, a 60-year-old approaching retirement. All on the same employer plan, all with a different reason to feel behind. The product had to mean something to all of them, on the same canvas, while the employer paid for it but never saw who used it.

Every feature traced back to a stat in the report.

The FWI measured four axes: knowledge, behaviour, perception, and productivity impact. I anchored the product to those four pillars and refused to ship a feature that didn't map to one of them. Discipline by design.

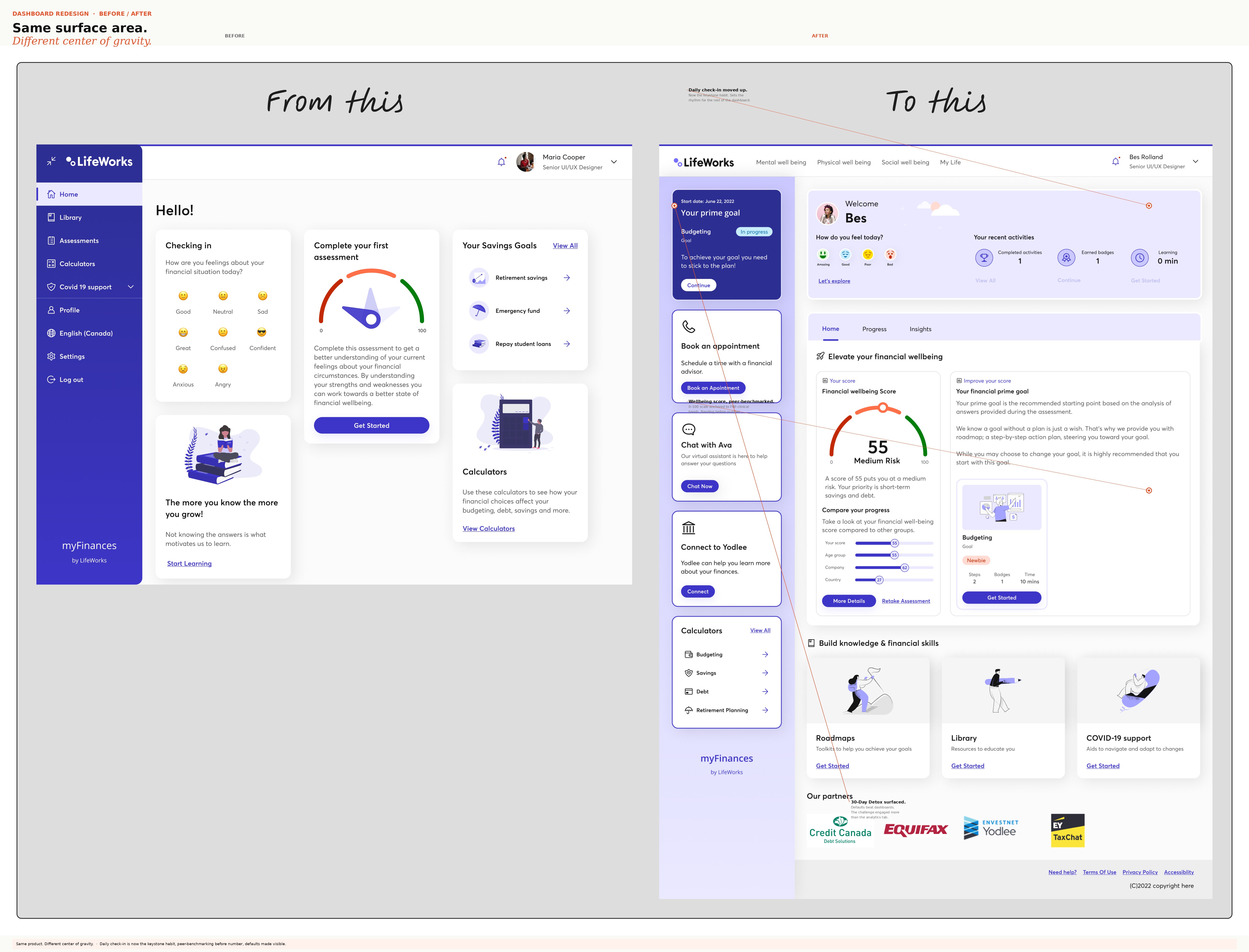

Working sessions ran weekly with the PM, the dev team, and the VP of Product. The hard conversations were not about UI. They were about scope, sequencing, and how loud to make privacy. I argued for fewer, simpler surfaces over a feature-heavy launch. We landed there.

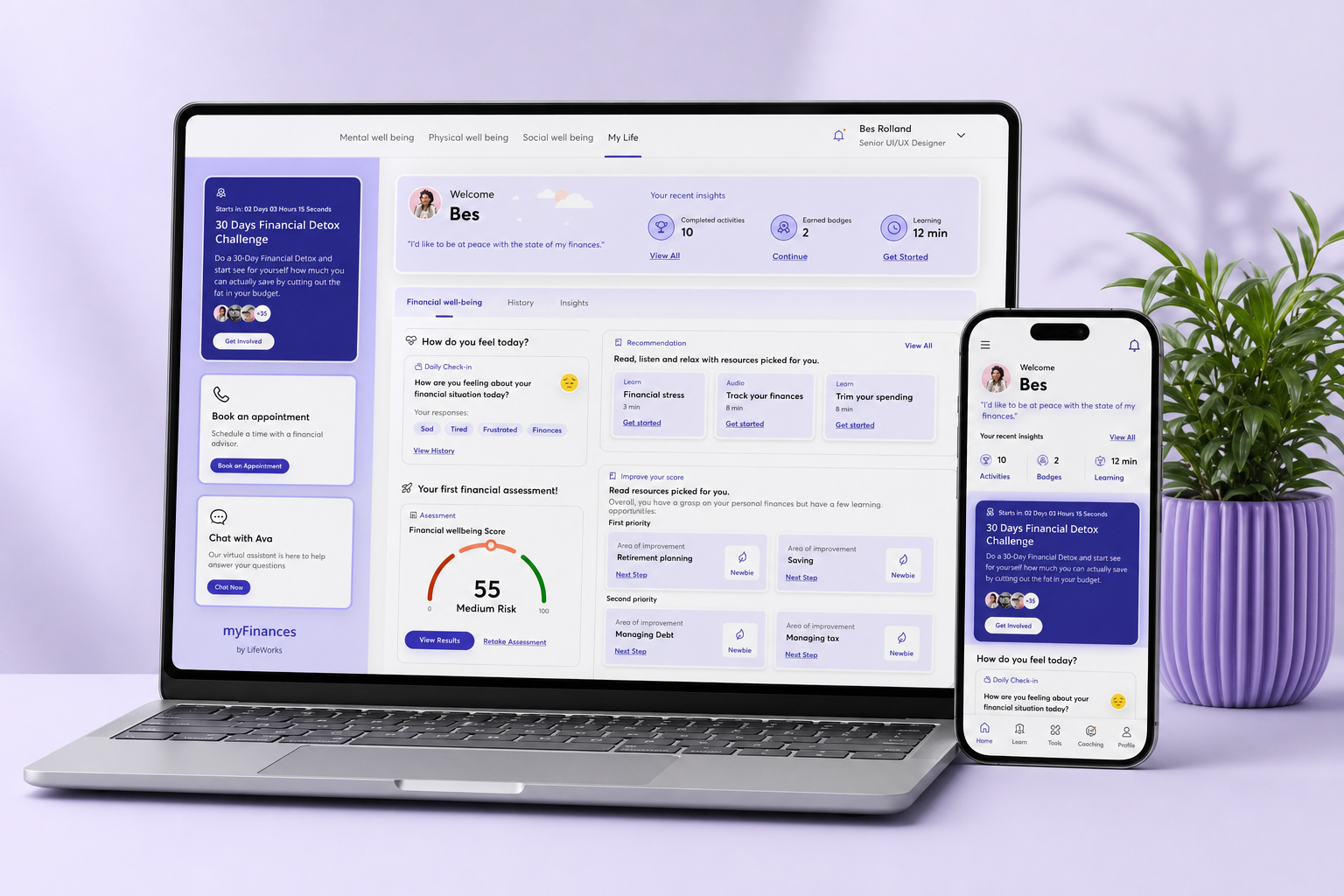

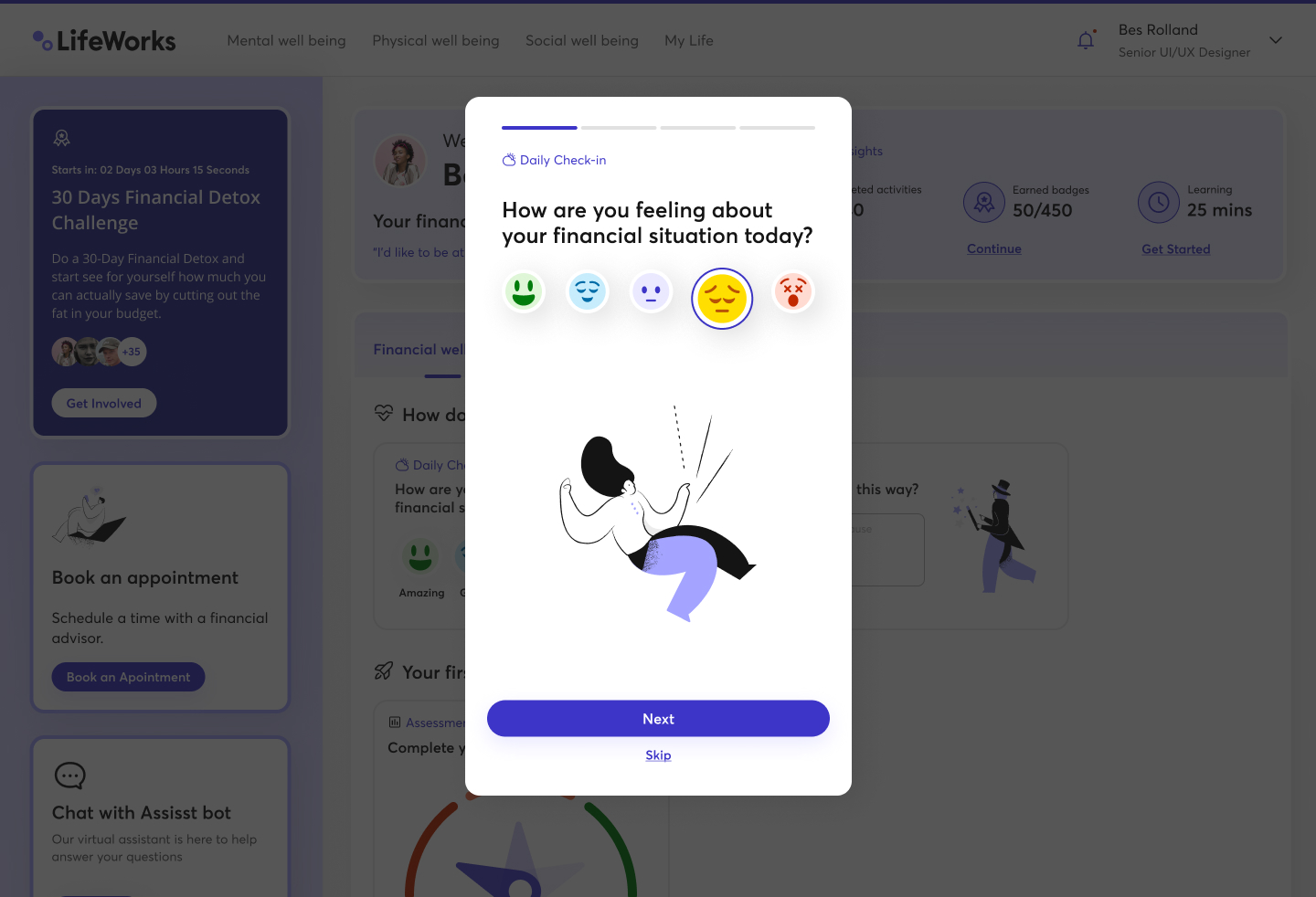

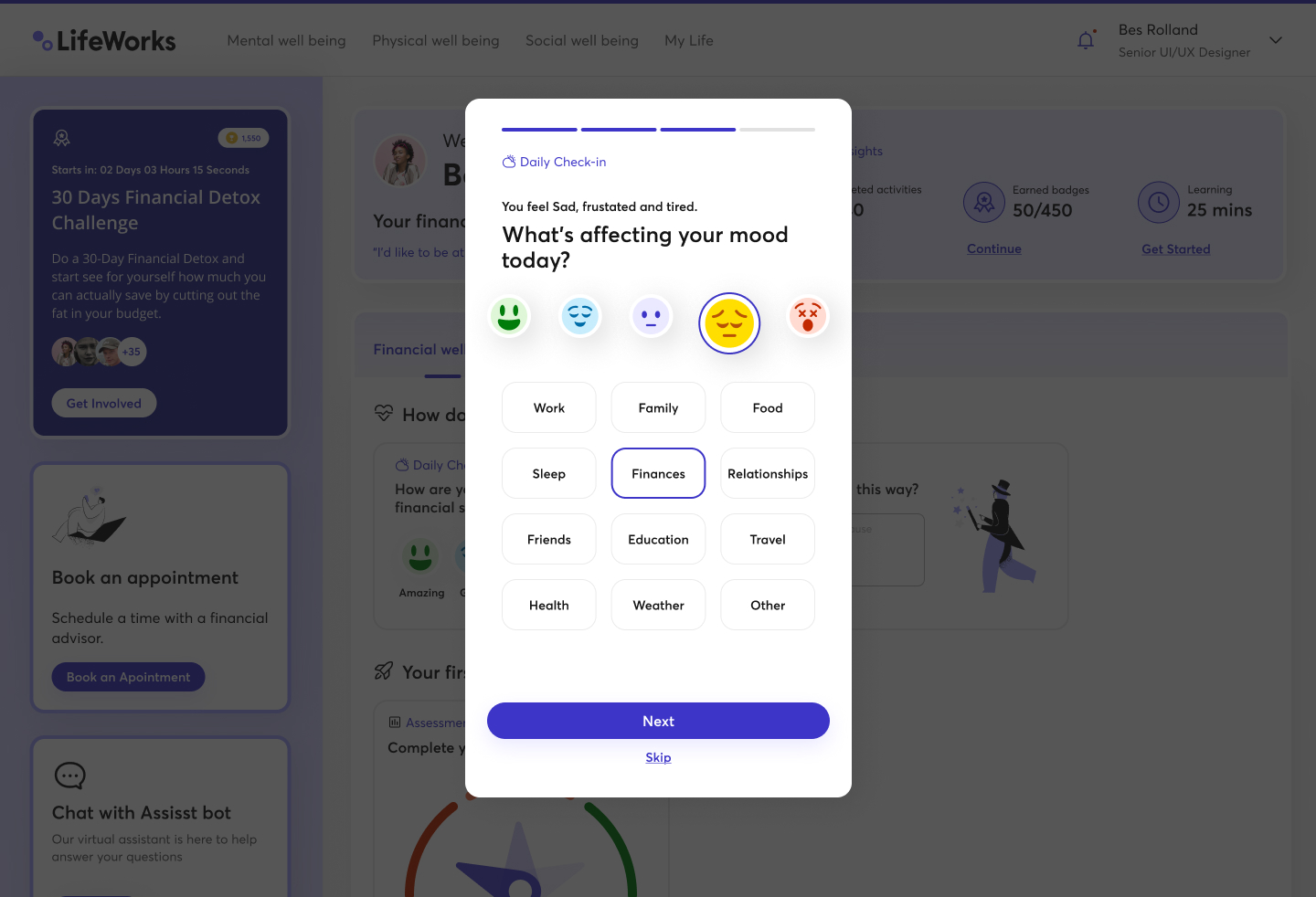

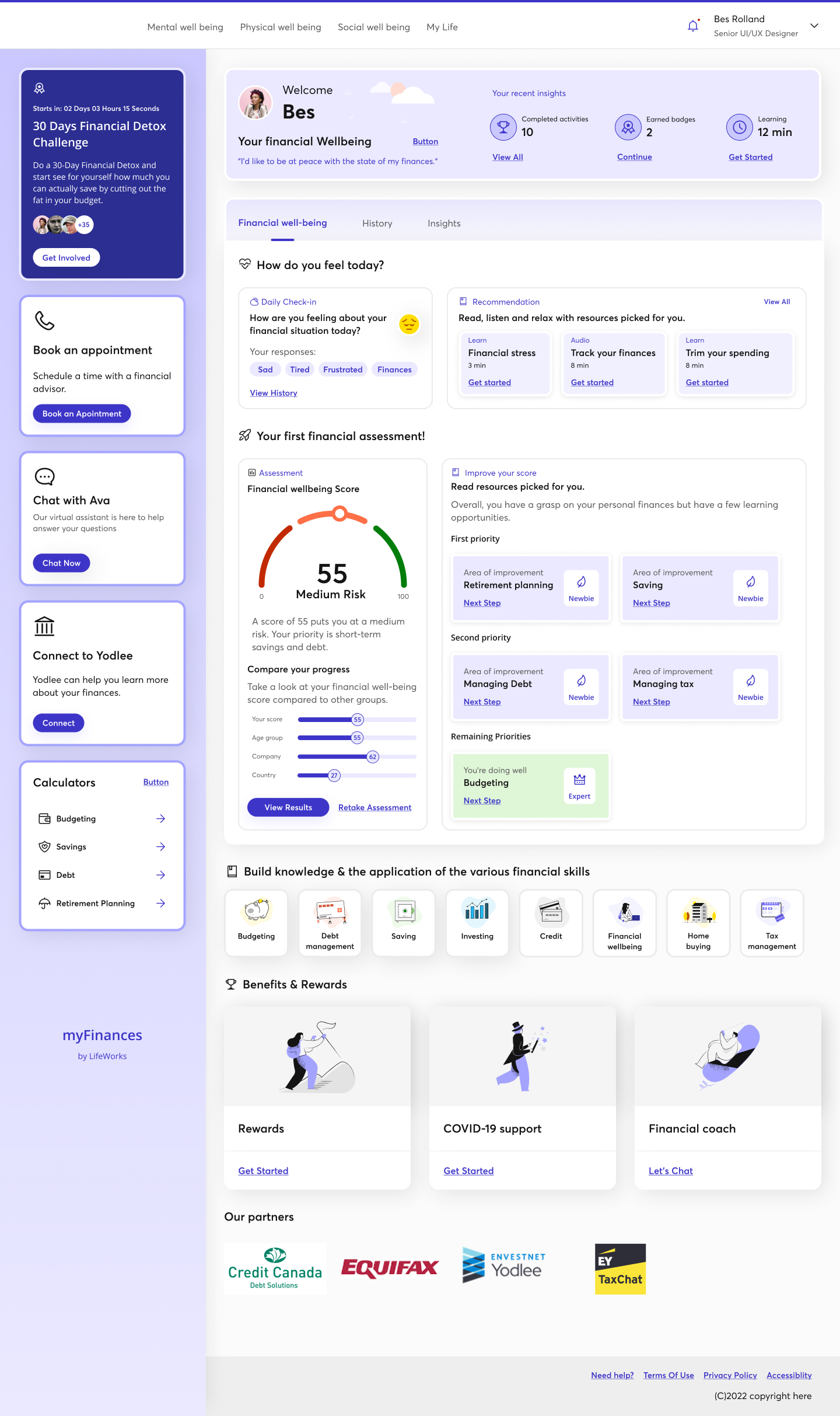

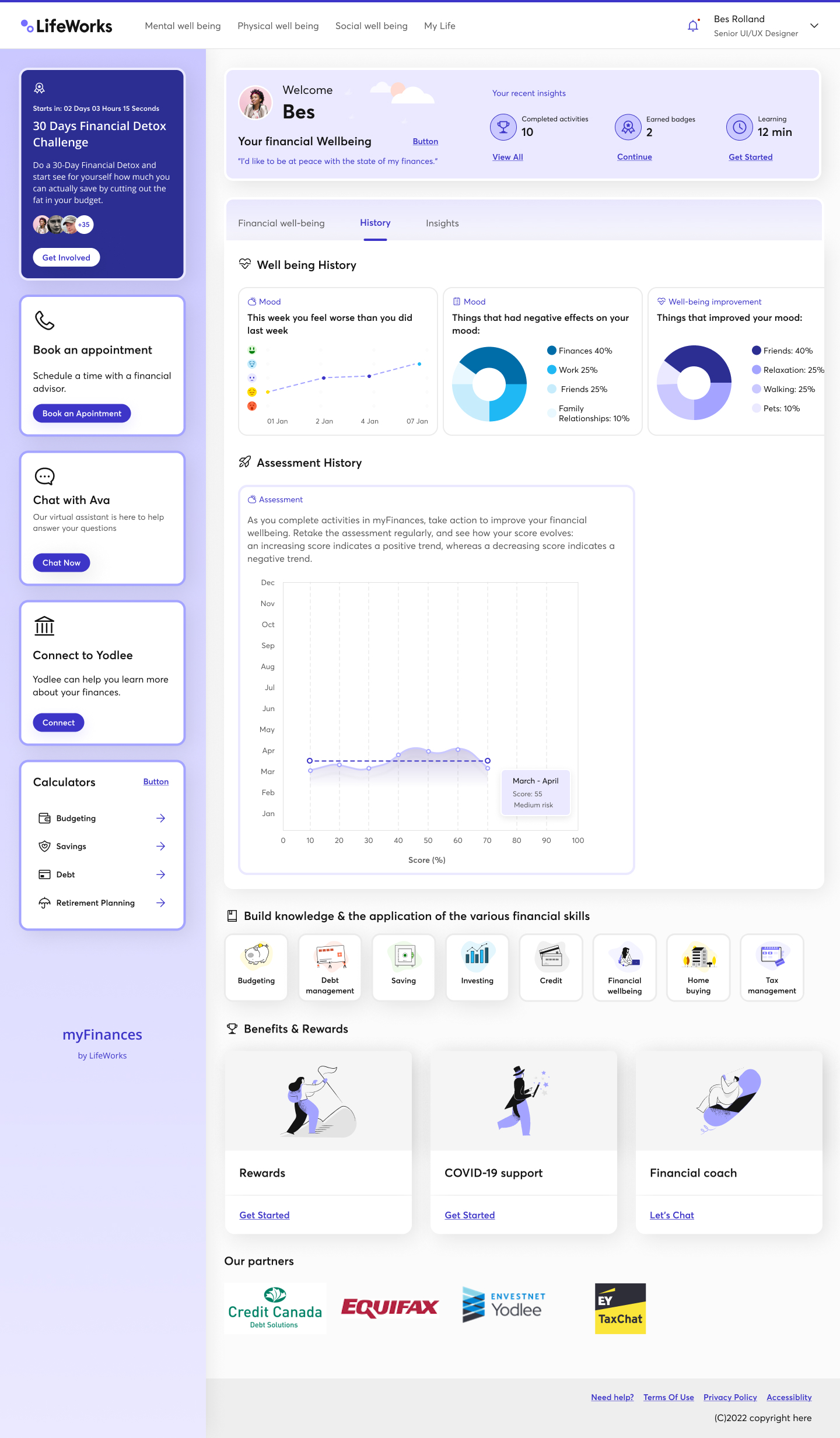

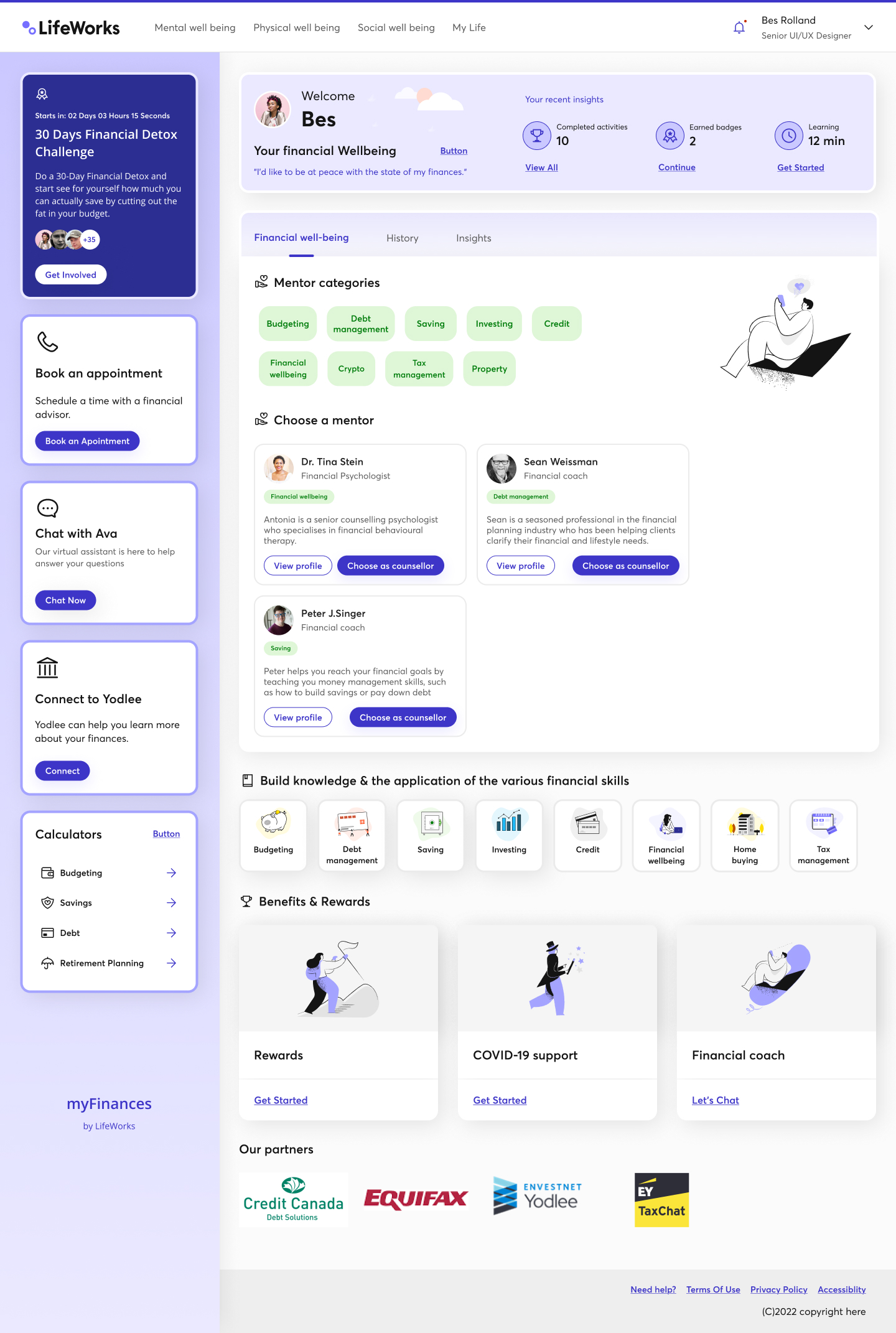

Seven surfaces from the shipped product.

Real screens from myFinances as it was built and demoed in 2022. Surfaces I owned end-to-end, from the assessment-based onboarding to the daily habit loop, the wellbeing score, the redesigned dashboard, and the mentor-booking flow.

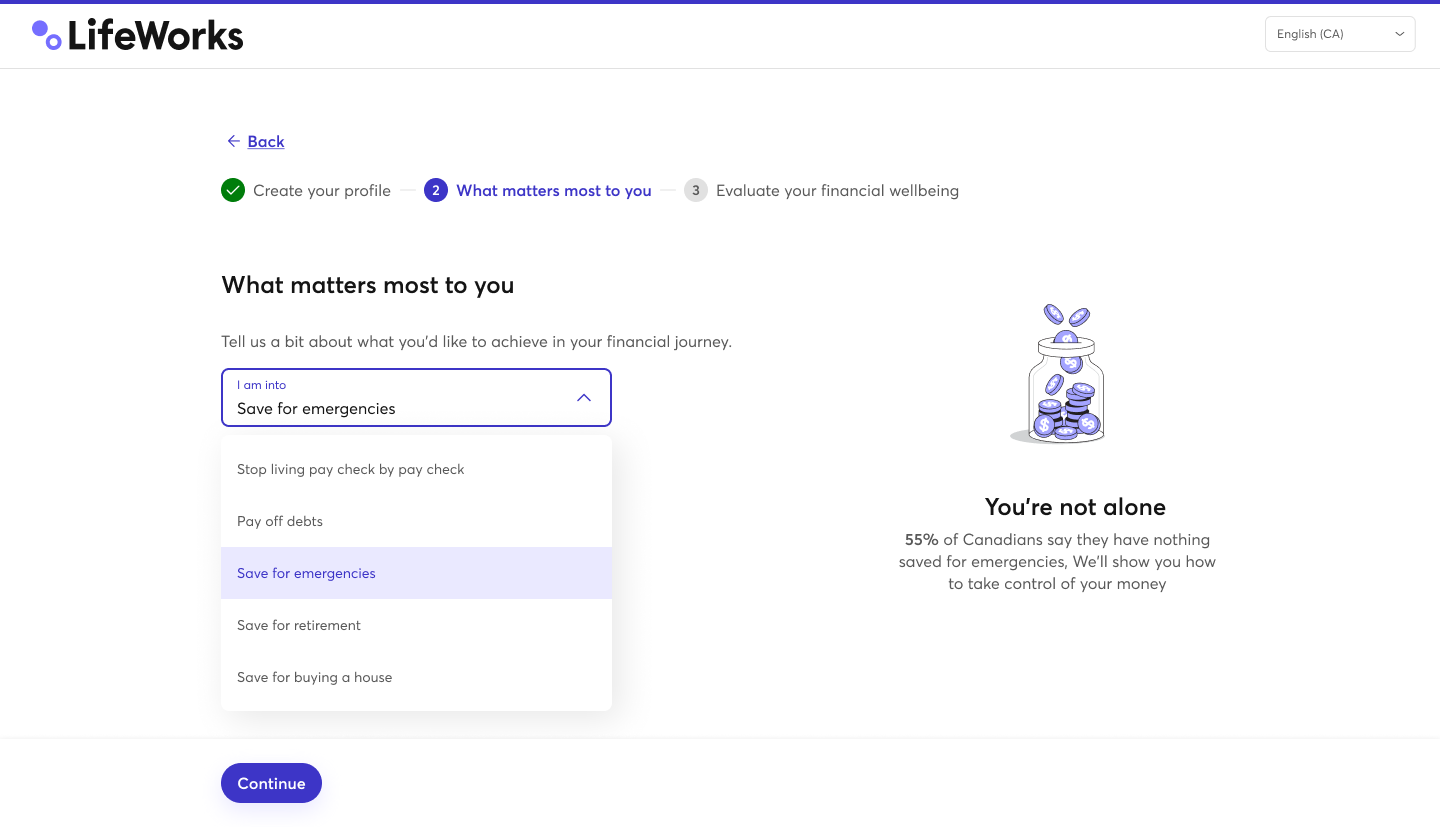

Walk through the shipped flows.

Two interactive prototypes: the full dashboard experience as it shipped to employees, and the assessment-based onboarding that sets the user's prime financial goal. Both desktop, both as designed and built in 2022.

Five decisions that shaped the product.

Directional, NDA-safe.

- Shipped to Canadian employees in 2022 as the third pillar of LifeWorks total wellbeing, sitting alongside the mental and physical wellbeing surfaces under one employer-funded login.

- Every shipped feature mapped to one of the four FWI sub-scores. The four-pillar framework (knowledge, behaviour, perception, productivity) became a recurring reference point with the PM, the dev team, and the VP of Product, and the spine of two later product proposals.

- The interactive prototypes I built were the demo asset the GTM team used when pitching the product to large Canadian employers.

- Score widgets, peer-benchmark rows, mentor cards, and assessment surfaces became the system the rest of the team built against, outlasting the product itself.

- “Your employer never sees this” was the most-screenshotted asset in usability sessions, and the line that turned the product from a B2B benefit into something employees trusted with personal data.

The four-pillar discipline, the research-to-product translation, and the privacy posture are what I carried with me into later work.

Three things I took with me.

Finance products over-design the rational layer and under-design the emotional one. You can't math your way out of how someone feels about money. But you can design around it, if every feature is tied to a number that proves it matters.